FTSE 100 - 2024

FTSE 100: Biodiversity & Nature

Author

Freddie Stretch

5 Nov 2024

This article is part of our ongoing series that leverages advanced LLM frameworks to assess the FTSE 100’s progress in ESG disclosures, focusing on climate and nature standards. In this article we dive into the status of Biodiversity and Nature reporting, the evolving regulatory landscape in the UK, and how this impacts stewardship teams.

History of Biodiversity Reporting

The Taskforce on Nature-related Financial Disclosures (TNFD) defines biodiversity and nature reporting as the process by which organisations disclose their impacts, dependencies, risks, and opportunities related to nature. This type of reporting goes beyond traditional energy, climate risk and GHG reporting. It provides insights into how a company’s activities interact with natural ecosystems, including biodiversity and water usage, and how these interactions may affect the organisation’s financial stability, sustainability, and long-term resilience.

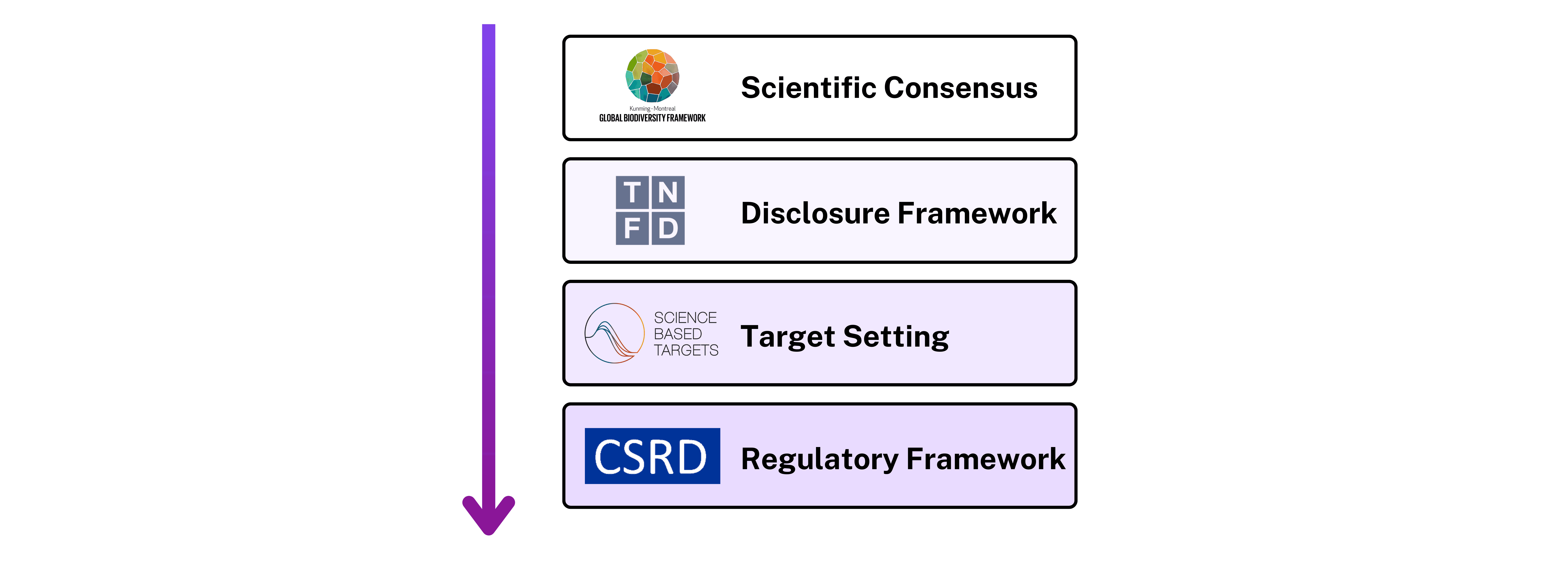

Biodiversity reporting has progressed significantly, reflecting growing awareness of the need for conservation and sustainable practices. The Kunming-Montreal Global Biodiversity Framework (GBF), agreed upon in 2022, has catalysed this shift by setting ambitious targets, such as protecting 30% of land and sea areas by 2030, reducing pollution, and mobilising finance for biodiversity. This framework has prompted businesses and financial institutions worldwide to consider the material risks and dependencies associated with nature and biodiversity loss.

In response, corporate reporting on biodiversity is being shaped by frameworks such as TNFD, Science-Based Targets for Nature (SBTN), and the Corporate Sustainability Reporting Directive (CSRD). Each of these frameworks has a unique focus, helping businesses assess, set targets, and disclose their impacts on ecosystems and biodiversity. TNFD provides a structure for identifying nature-related risks and opportunities, SBTN focuses on setting science-based nature targets, and CSRD mandates disclosures on biodiversity, pollution, resource use and water impacts under EU regulation. Together, these frameworks create a roadmap for companies to translate global biodiversity goals into corporate actions, pushing for transparency and accountability in nature-related performance.

Results of FTSE 100 Analysis

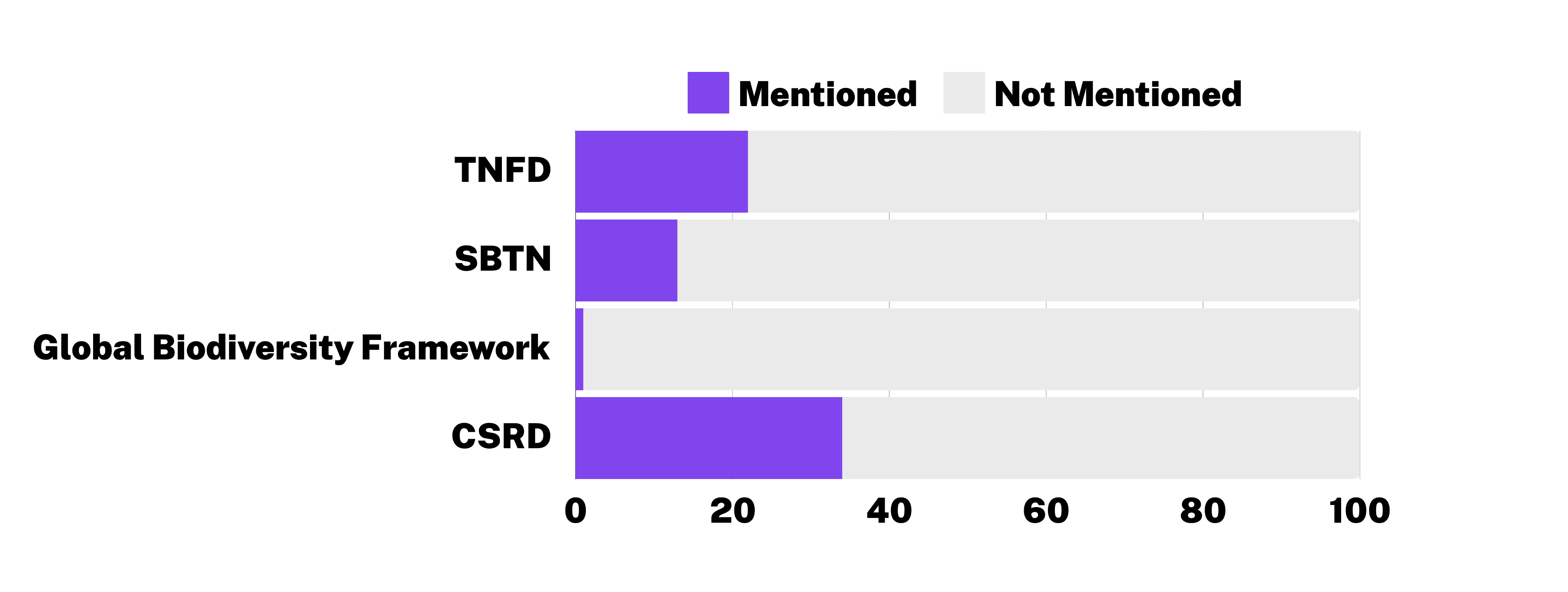

Our analysis of the FTSE 100’s nature-related reporting reveals a mix of progress and gaps. The first graphic (above) highlights how many companies have started reporting on TNFD. Although 500 companies worldwide have committed to TNFD as of COP 16 in October 2024, current uptake within the FTSE 100 remains limited. This is partly because TNFD is relatively new compared to well-established climate-focused frameworks. While TNFD is gaining traction, there’s a long journey ahead for it to achieve the same maturity level as climate risk and greenhouse gas (GHG) reporting frameworks.

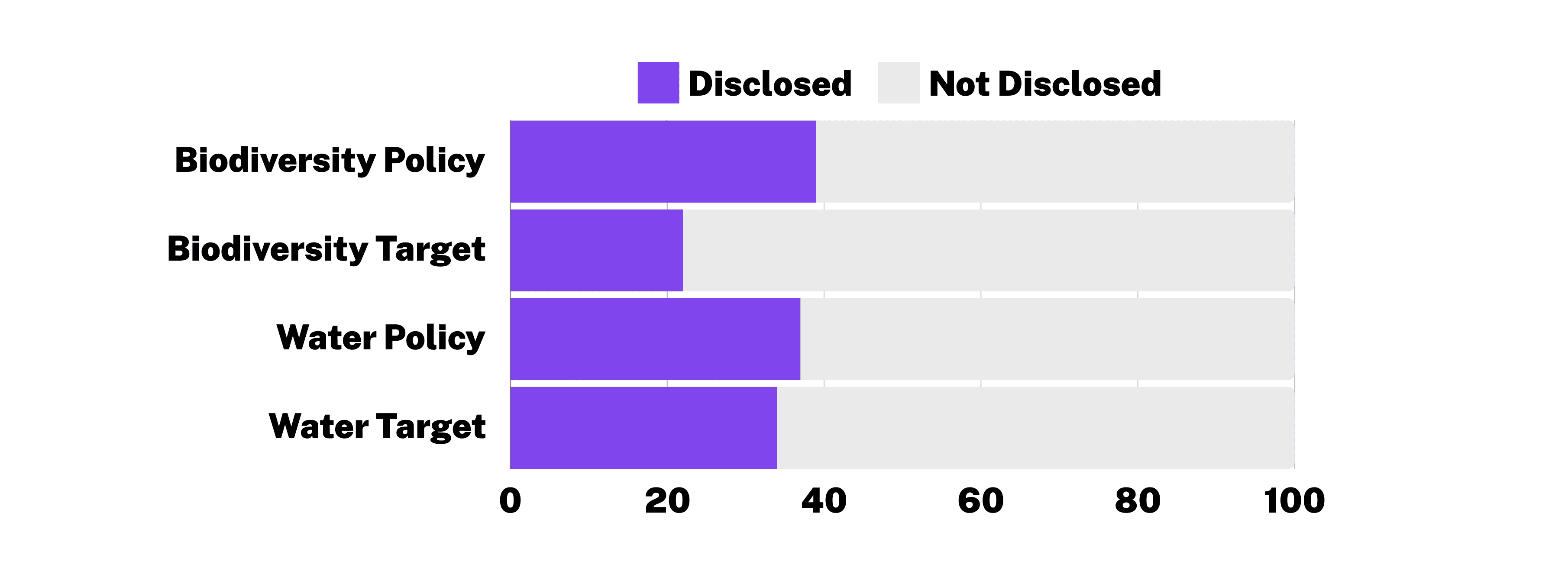

This second graphic indicates how the adoption of biodiversity and water policies among the FTSE 100 is already reasonably high, despite a lack of standardisation, with 37 companies having both water and biodiversity policies. Yet, even many of those with a policy, still haven't created targets for reducing their impact. Also, standardised and substantive action remains limited until they all take up TNFD, underscoring the need for further development and uniformity in corporate biodiversity reporting.

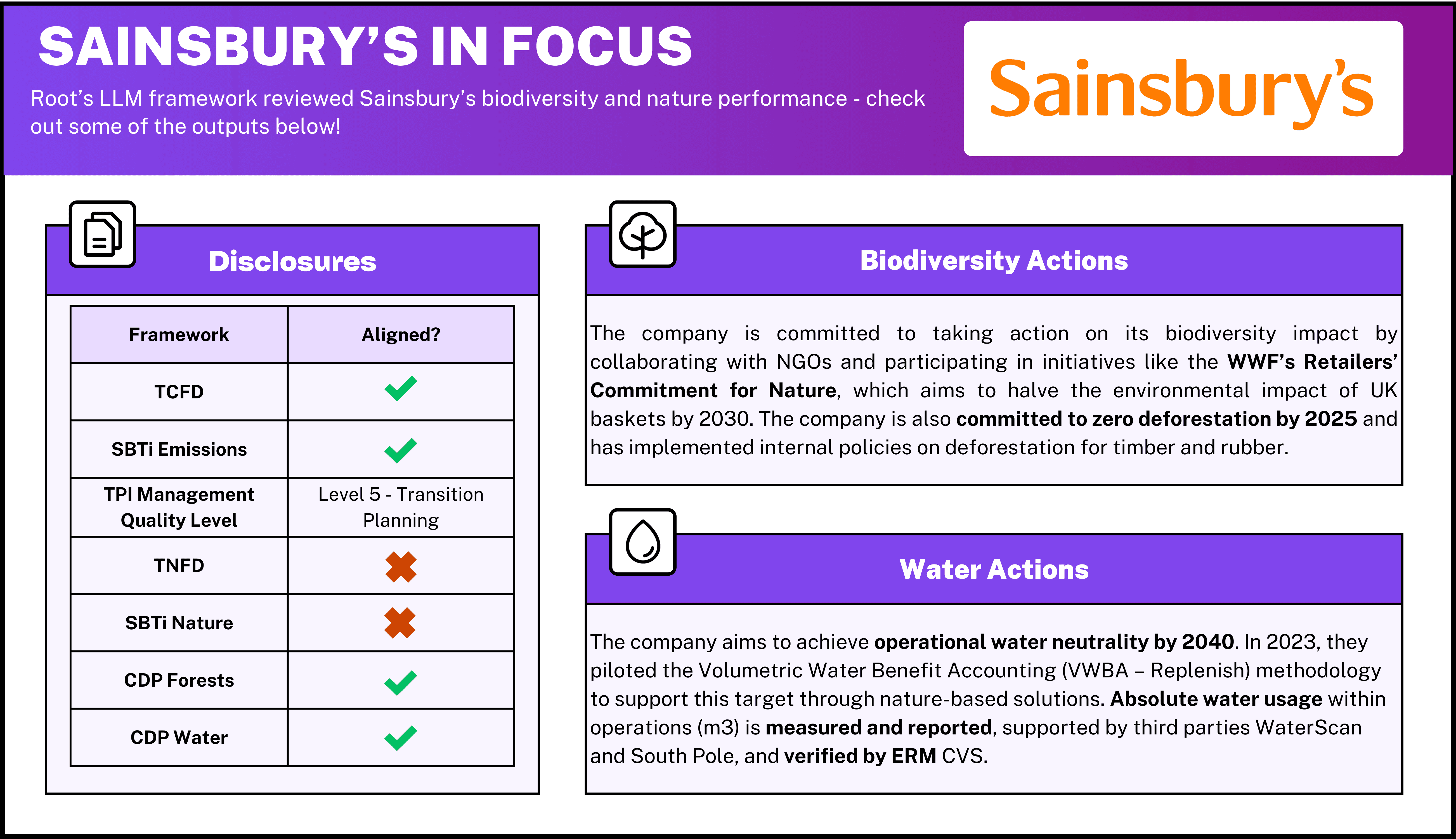

Case Study: Sainsbury’s in Focus

Our Sainsbury’s case study below offers an illustrative example of how a major corporation is navigating the landscape of biodiversity and nature reporting. Root’s LLM framework assessed Sainsbury’s biodiversity and nature-related performance, providing an analysis of what it is already doing to tackle its impact on nature.

While Sainsbury’s shows positive actions, it also highlights the need for greater standardisation in nature and biodiversity reporting, it mentions TNFD in its reporting, but still needs to fully implement this framework to its operations. However by engaging with CDP and TCFD, it has already made great strides in understanding and taking action on its climate impact. The content of this report was produced by Root's LLM framework, which we apply to 1,000s of companies to support stewardship teams find gaps in their portfolio and inform their engagement actions.

Future for Stewardship of Nature

Looking forward, the stage is set for substantial advancements in nature-related reporting and corporate accountability, driven by investor expectations and emerging frameworks. With 500 companies already committed to TNFD, the path forward will require robust reporting, clear targets, and strong investor engagement to accelerate progress.

Investor expectations are also evolving, with initiatives like Nature Action 100+ and the Forest 500 campaign rallying investors to demand more from companies on nature-related actions. These initiatives create additional pressure for companies to close existing knowledge gaps, improve data availability, and adopt nature-based benchmarks.

While progress is evident, corporate nature reporting is still nascent. Many companies face knowledge gaps, limited data availability and inconsistent benchmarks to measure biodiversity impacts accurately. This leaves stewardship teams navigating complex landscapes with limited actionable data on biodiversity, posing challenges for corporate accountability.

To support investors and stewardship teams, Root offers specialised tools, including resolution intelligence and benchmarking analyses. Root’s LLM frameworks help teams identify disclosure gaps, benchmark companies against standards like Nature Action 100+, and gauge high-risk areas within portfolios. These insights enable investors to engage meaningfully on nature issues, advocating for robust biodiversity strategies that align with emerging standards and benchmarks.

Disclaimer: The data content is generated using Generative AI and Large Language Models (LLMs), which may introduce inaccuracies. Our FTSE 100 series analysis focuses solely on the annual reports of these companies. It is important to note that some companies may publish additional information on their ESG disclosures and strategies in other reports not covered in this analysis. Therefore, this analysis should not be considered a comprehensive or definitive source of information.